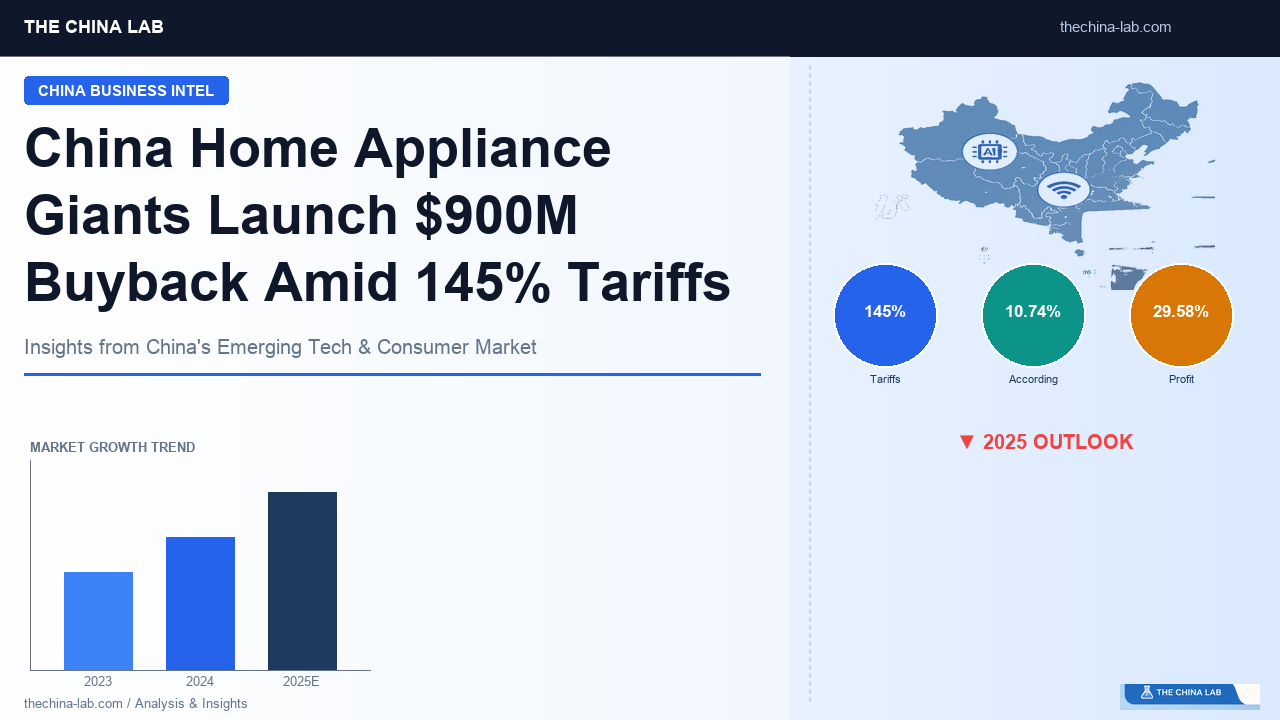

China Home Appliance Giants Launch $900M Buyback Amid 145% Tariffs

Why This Matters Now

In April 2025, US-China tariff tensions reached a critical threshold. US tariffs on Chinese goods climbed to a cumulative 145%, while China retaliated by raising duties on American products to 125%.

Yet amid this trade war escalation, Chinese home appliance and smart home companies made a surprising move that caught market attention: massive share buybacks. Within a single week (April 4–11), nine companies announced buyback programs totaling up to 4.5 billion yuan ($900 million).

Why would companies invest their own capital during such turbulent times? Understanding this strategic decision reveals the underlying strength and future direction of China’s smart home industry.

Share Buybacks: The Strongest Confidence Signal

Midea’s 3 Billion Yuan, Haier’s 2 Billion Yuan — What the Numbers Mean

According to a Guoyuan Securities report, Midea Group led this buyback wave. China’s largest home appliance manufacturer announced a buyback program of up to 3 billion yuan ($600 million). The company stated that acquired shares would fund equity incentive programs and employee stock ownership plans — signaling a focus on long-term value creation rather than short-term stock price defense.

Haier Smart Home followed with a buyback program of up to 2 billion yuan. Additionally, the company’s directors and senior executives personally purchased over 20 million yuan in additional shares. When executives invest their own money in company stock, it represents one of the most credible signals of confidence in business performance.

Why Buybacks Signal Bullishness

Share buybacks typically indicate several key factors:

- Management believes the stock is undervalued

- Strong cash flow and healthy balance sheet

- Commitment to shareholder returns

- A clear message to the market: “This company is resilient”

The timing makes these buybacks particularly significant. Executing them during peak external pressure — tariff escalation and market volatility — demonstrates genuine conviction. The Guoyuan report describes this as companies “communicating confidence with real money,” emphasizing these aren’t performative gestures.

Are Fundamentals Really Solid? — 2024 Performance Data

28 Companies Combined: Revenue +9.49%, Net Profit +10.74%

According to the report, as of April 12, 2025, 28 of 103 listed home appliance companies had disclosed full-year 2024 results. The aggregate figures paint a positive picture:

| Metric | Amount | Year-over-Year Change |

|---|---|---|

| Total Revenue | 1.01 trillion yuan ($200 billion) | +9.49% |

| Net Profit (attributable to parent) | 74.7 billion yuan ($15 billion) | +10.74% |

Among these 28 companies, 23 achieved revenue growth and 13 reported profit increases. Despite US-China friction and consumer market uncertainty, the industry maintained steady growth momentum.

Individual Company Performance

- Midea Group: Revenue 409 billion yuan (+9.47%), Net profit 38.5 billion yuan (+14.29%)

- Haier Smart Home: Revenue 285.9 billion yuan (+4.29%), Net profit 18.7 billion yuan (+12.92%)

- TCL Home Appliances: Revenue 18.3 billion yuan (+20.96%), Net profit 1 billion yuan (+29.58%)

TCL Home Appliances’ 29.58% profit growth stands out. Mid-sized growth companies improving profitability are helping support the broader industry recovery.

Domestic Policy Tailwinds — The Trade-In Program Effect

While tariffs pressure exports, the Chinese government has strengthened domestic demand stimulus measures.

Subsidy Coverage Expanded from 8 to 12 Product Categories

In early 2025, China’s National Development and Reform Commission and Ministry of Finance announced an expansion of home appliance trade-in subsidies from 8 to 12 product categories.

The results are evident in the data:

- 2024 Trade-In Program Results: Over 62 million units of appliances sold across 8 categories, directly boosting consumption by approximately 270 billion yuan

- January 1 – April 8, 2025 Results: In just over three months, 12 categories generated 35.7 million unit sales and 124.7 billion yuan in consumer spending

Furthermore, the home appliance industry’s January–February 2025 performance showed operating revenue up 9.9% year-over-year and total profits up 10.3%, reflecting early policy effectiveness.

Investment and Business Implications

Market Positioning Insights

China’s smart home industry currently benefits from three simultaneous growth drivers:

- Rapid AI and IoT technology deployment (Huawei HarmonyOS-enabled smart home ecosystems)

- Aging population demand (fall detection sensors, monitoring systems, elderly-friendly products)

- Strong government subsidy programs

The industry is shifting from “standalone smart appliances” to “whole-home intelligence” — a fundamental transformation that creates significant opportunities across the value chain.

Strategic Considerations for International Businesses

Supply Chain Adaptation: Major Chinese appliance manufacturers have established overseas production facilities to create “tariff-avoidance supply chains.” International companies may explore partnerships with Chinese firms for third-country manufacturing arrangements.

Elderly-Focused Smart Home Products: Both China and Japan face significant population aging challenges. This creates natural collaboration opportunities in product development and technology licensing for senior-friendly smart home solutions.

Investment Timing Signal: The buyback wave may indicate a stock price floor for Chinese home appliance companies. Investors monitoring China market entry points should track whether these programs stabilize valuations.

Technology Partnership Opportunities

The convergence of AI sensors, caregiving technology, and residential infrastructure represents a particularly promising area for international collaboration. Chinese companies bring scale manufacturing and domestic market access, while international partners often contribute specialized technology and global distribution networks.

Companies with expertise in voice recognition, computer vision for in-home monitoring, or energy management systems may find receptive partners among China’s major appliance manufacturers seeking to differentiate their smart home offerings.

Key Takeaways

-

Despite 145% US tariffs, Chinese home appliance giants demonstrated industry confidence through share buybacks. Midea committed 3 billion yuan, Haier 2 billion yuan, with nine companies totaling 4.5 billion yuan in capital returns.

-

2024 industry performance remained solid with revenue growth of 9.49% and net profit growth of 10.74%. The expanded trade-in subsidy program (now covering 12 categories) generated 124.7 billion yuan in consumer spending within the first three months of 2025.

-

Smart home industry growth rests on three pillars: AI/IoT technology integration, aging population demand, and government subsidy policies. The shift toward “whole-home intelligence” creates significant business opportunities for both domestic and international players.

→ Related: China Smart Home Market Trends | China AI Industry Report | AWE 2026 Highlights

Leave a Reply