China Smart Home Market Hits 1 Trillion Yuan: AI, Silver Economy Drive Growth

Why the China Smart Home Market Demands Attention Now

In 2025, the combined revenue of China’s 28 publicly listed home appliance companies reached 1.014 trillion yuan (up 9.49% year-over-year)—equivalent to approximately $140 billion USD. This milestone represents far more than market scale alone.

The home appliance sector—traditionally viewed as a mature industry—has entered a new growth trajectory powered by three engines: mass AI deployment, a 220-million-strong senior consumer base, and aggressive global expansion strategies.

Net profits across the sector climbed to 87.6 billion yuan (up 13.2%), while home appliance stocks gained 9.1%, reflecting strong institutional investor confidence. Yet many international business professionals continue to watch on the sidelines, underestimating the transformation underway.

This analysis examines the most significant development reshaping China’s smart home market: the convergence of the silver economy and AI-enabled appliances—and what it means for international businesses and investors.

The Silver Economy: A Trillion-Yuan Blue Ocean

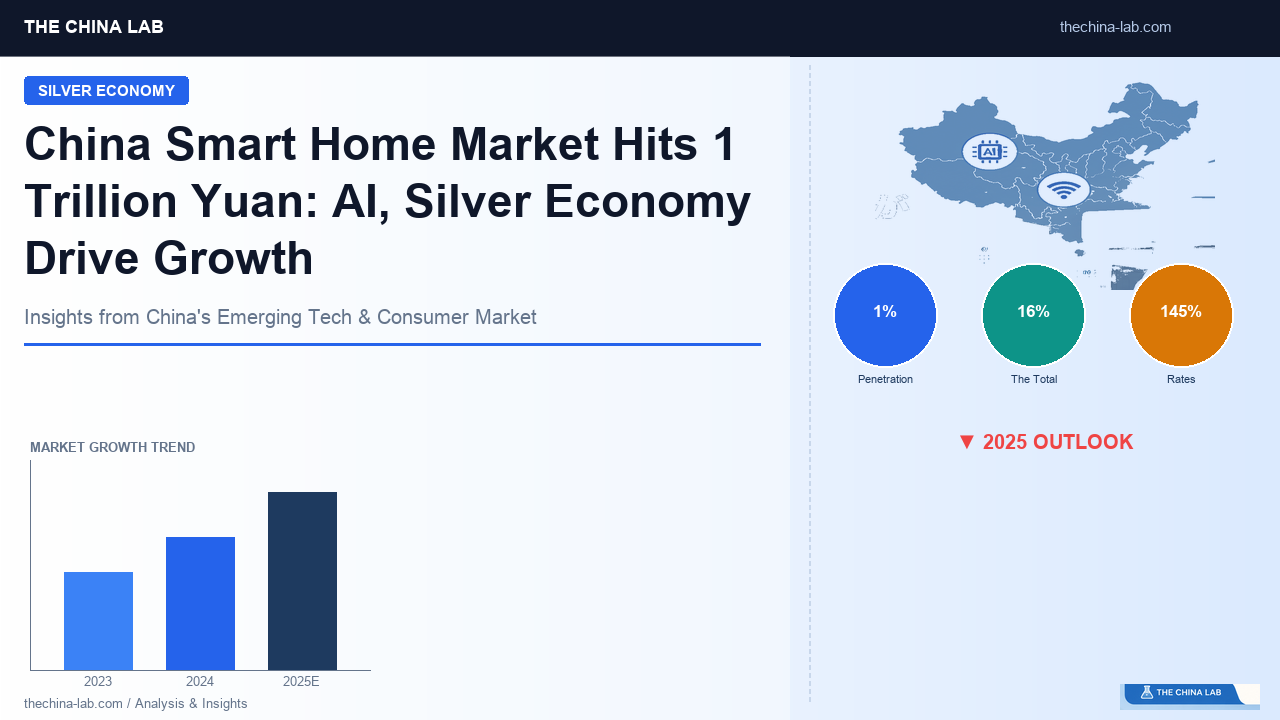

220 Million Seniors, Sub-1% Penetration Rates

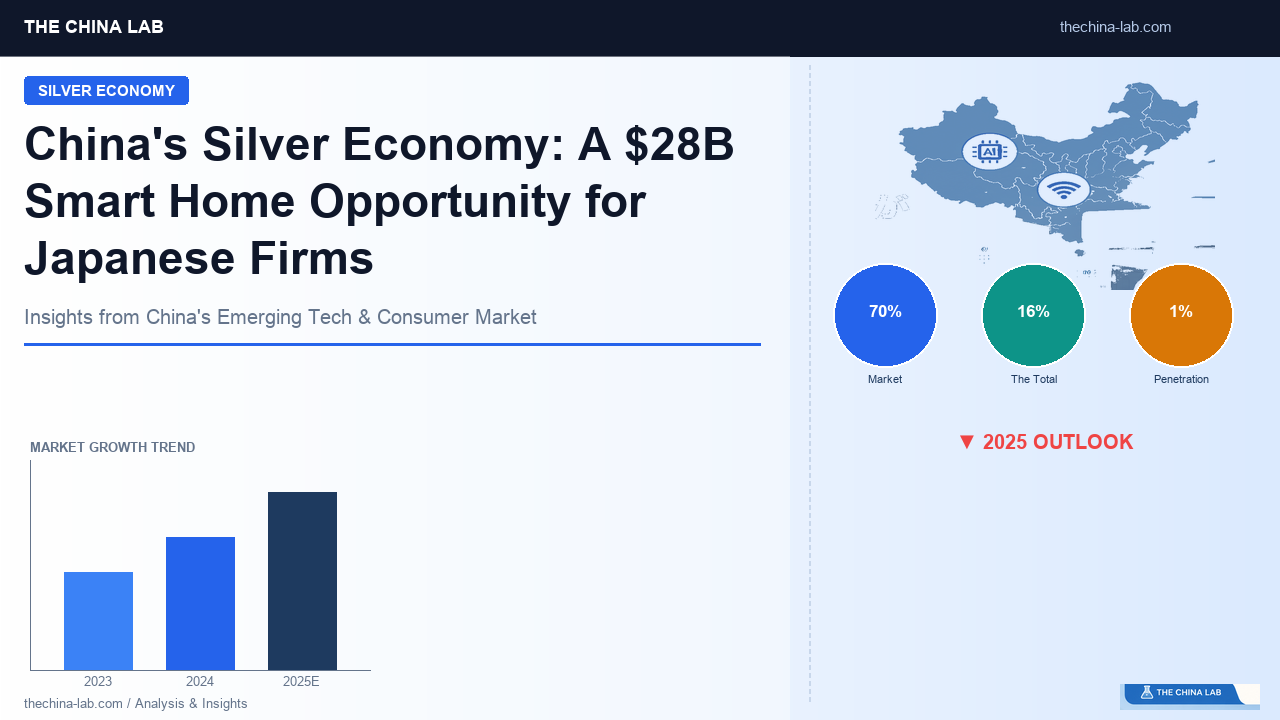

China’s population aged 65 and above currently stands at 220 million people (16% of the total population). By 2035, this figure is projected to exceed 400 million. This massive demographic shift is creating unprecedented opportunities in the smart appliances × healthcare and eldercare segment.

Consider this striking data point: The market penetration rate for AI-enabled smart mattresses (known as AI床垫 or smart beds) currently sits at less than 1%.

This translates to vast untapped potential in which first movers can capture outsized returns.

DeRUCCI, a leading rest technology brand, demonstrated this opportunity vividly. In the first half of 2025, the company’s AI product sales grew more than threefold year-over-year to 121 million yuan. Triple-digit growth in a sub-1% penetration market illustrates precisely what early entrants can achieve when timing market emergence correctly.

Three Core Demand Categories

Senior consumer demand in the appliance sector clusters around three primary needs:

| Need Category | Representative Products | Current Penetration |

|---|---|---|

| Health Monitoring | AI smart beds, blood pressure-integrated devices | Below 1% |

| Daily Living Support | Care robots, voice-controlled interfaces | Low |

| Safety & Surveillance | AI cameras, smart locks | Medium |

The long-term market size for care robots alone is estimated to exceed 200 billion yuan, with 2027–2028 identified as the inflection point for mainstream adoption.

Why 2027–2028 Marks the Turning Point

Three converging factors explain this timeline:

- Demographic structure: China’s equivalent of the baby boom generation will reach age 75 and above, triggering a surge in care-related demand

- Technology maturity: AI sensors and voice recognition will achieve the accuracy levels required for mass consumer adoption

- Policy support: Government silver economy initiatives will materialize as concrete subsidies and regulatory frameworks

Three Numbers That Define the Market

Beyond the silver economy, several key metrics are essential for understanding China’s smart home market trajectory in 2025–2026.

1. Trade-In Program: +38.8% Single-Month Growth

The government’s appliance replacement subsidy program (以旧换新) expanded past 8 product categories in 2024 to 12 categories in 2025. Cumulative sales impact since January through April 2026 reached 51 million units worth 174.5 billion yuan, with April alone recording a 38.8% year-over-year increase in home appliance retail sales.

This policy clearly functions as a market floor, supporting baseline growth. However, businesses should factor in potential demand pullback when subsidies eventually phase out.

2. AI Appliances: Six Categories Enter Mass Production

AI integration has transitioned past concept to commercial scale across six product categories:

- Imaging and drones (Insta360 achieved 30,000 unit sales in its launch month)

- Office and AI NAS (home storage devices with integrated LLM capabilities)

- AI translation earbuds

- AI security cameras

- Residential AI energy storage systems

- Smart glasses (2026 designated as the first year of mainstream adoption)

Xiaomi’s home appliance sales surged over 100% year-over-year, demonstrating how AI integration has become a primary growth engine for leading brands.

3. US-China Tariffs: 145% Rates Accelerate Global Expansion

US tariffs on Chinese goods have reached as high as 145%, while Chinese retaliatory tariffs stand at 125%. These trade barriers are pushing Chinese manufacturers toward Southeast Asia, Europe, and the Middle East.

Midea and Haier are simultaneously pursuing ASEAN-routed production and direct US manufacturing investments. Hisense continues leveraging its FIFA sponsorship to build brand presence in European markets.

Strategic Implications for International Businesses

Career Opportunities

The transformation of China’s smart home market is creating significant opportunities for professionals with specific skill sets.

High-demand profiles include:

- Eldercare technology specialists: Experience in care-focused UX design and universal design principles—developed through decades of addressing Japan’s aging society—translates directly to China’s silver economy market. Both Japanese and Chinese manufacturers are actively seeking this expertise

- AI appliance product managers: Professionals capable of designing whole-home smart ecosystems are in high demand at Huawei, Xiaomi, and Midea’s global divisions

- Global expansion consultants: Professionals with established sales channels in Japan and ASEAN markets represent scarce, high-value resources for Chinese companies pursuing international growth

Business Entry Strategies

Industry analysis identifies four viable approaches for international companies:

| Strategy | Description | Complexity |

|---|---|---|

| A: Component Supply | High-value precision components, sensors, inverters | Medium |

| B: Silver Economy Solutions | Care equipment, medical devices, universal design products | Medium-High |

| C: Technology Licensing | Energy efficiency, air purification, specialty materials | Low-Medium |

| D: Global Expansion Partnership | Leveraging established sales channels for Chinese brand distribution | Low-Medium |

Strategy B (Silver Economy Solutions) represents the strongest differentiation opportunity for international companies. Markets with advanced aging populations possess 30+ years of accumulated expertise in eldercare and universal design. The sub-1% penetration AI mattress market and the 200+ billion yuan care robot opportunity represent ideal arenas for deploying this advantage.

Three pitfalls to avoid:

- Direct competition with Chinese manufacturers in mid-to-low price segments

- Over-reliance on government trade-in subsidies for product or sales strategy

- Technology disclosure to Chinese partners without robust contractual protections

Key Takeaways

-

China’s smart home appliance market has reached the 1 trillion yuan milestone, with net profit growth of 13.2% signaling a shift toward qualitative growth. AI mass production is advancing simultaneously across all major categories

-

The silver economy (220 million consumers aged 65+) represents the last major blue ocean for AI appliances. With smart mattress penetration below 1%, the 2027–2028 period marks the critical inflection point for market expansion

-

The winning strategy for international companies lies not in price competition but in leveraging high-value capabilities—eldercare UX expertise, energy efficiency technology, and precision sensors—through silver economy solutions or component supply partnerships

→ Related: China Smart Home Market Trends | China AI Industry Report | AWE 2026 Highlights

Leave a Reply