China’s Smart Home Appliance Dominance: From Volume to Value

Why China’s Smart Appliance Market Demands Attention Now

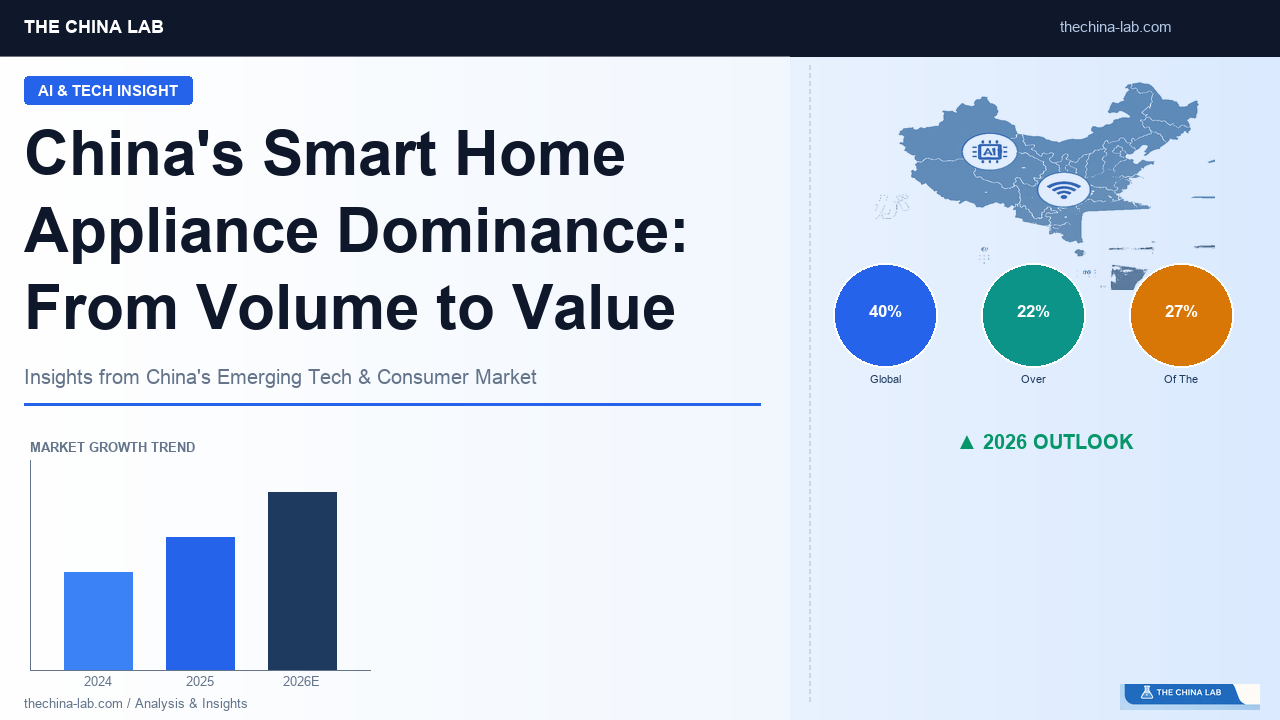

The global smart home appliance market reached approximately $147.5 billion in 2025. Growing at a remarkable compound annual rate of 22% over the past decade, the market is projected to surpass $180 billion in 2026.

China sits firmly at the center of this expansion. Chinese brands now command 38–40% of global shipments by volume, securing the top position worldwide. But this is no longer just a story of cheap mass production. AI-powered robot vacuums from Chinese manufacturers have captured leading global market share, while premium kitchen appliance makers are establishing proprietary technology brands that compete on innovation rather than price alone.

For business professionals and investors watching Asian markets, this shift presents a complex mix of competitive threats, partnership opportunities, and investment potential. Drawing on a comprehensive industry analysis from Zhongyuan Securities (March 2026), this article examines the most significant development: the vast “smart home gap” within China’s domestic market and the competitive strategies Chinese companies are deploying to capture it.

The Surprising Gap in China’s Domestic Market

China vs. America: A Tale of Uneven Adoption

The assumption that China leads universally in smart home adoption doesn’t hold up under closer examination. Penetration rates vary dramatically by product category. Consider the 2025 household penetration figures for key smart appliance segments:

| Product Category | China | United States |

|---|---|---|

| Smart Refrigerators | 8% | 8% |

| Robot Vacuums | 4.2% | 15% |

| Dishwashers | 5% | 39% |

| AI Kitchen Appliances | 24% | 59% |

While smart refrigerator adoption runs parallel in both markets, robot vacuum penetration in the U.S. exceeds China’s by 3.6 times, and dishwasher penetration by nearly 8 times. This paradox is striking: China produces 27% of the world’s robot vacuums yet has deployed them in only 4.2% of its own households.

Robot Vacuums: The Hottest Domestic Blue Ocean

This apparent contradiction reveals the largest business opportunity in China’s smart home sector.

According to IDC data, the global robot vacuum market reached 24.12 million units shipped and $11.5 billion in sales in 2025—a 23% year-over-year increase. Meanwhile, China’s domestic household penetration of 4.2% is forecast to nearly double to 7.6% by 2029, representing potential additional demand of tens of millions of units from the domestic market alone.

Chinese brands already dominate global shipments:

- Roborock (石头科技): 5.8 million units, 17.7% share, +76.5% YoY

- Ecovacs (科沃斯): 4.7 million units, 14.3% share, +38.3% YoY

- Dreame (追觅): 3.4 million units, 10.5% share, +101.9% YoY

- Xiaomi (小米): 2.2 million units

- Narwal (云鲸): 1.7 million units

The top five Chinese brands account for over 50% of global shipments. Roborock alone holds approximately 18% of the worldwide market.

Dishwashers: Signs of Explosive Growth

The dishwasher segment warrants close attention. China’s 5% household penetration pales against Germany’s 90% and America’s 39%. However, dishwasher transaction volume in January 2026 surged 69% year-over-year, with participating brands expanding to 101 companies. These indicators suggest the market is entering a genuine takeoff phase.

From Volume Leader to Margin Leader: The Gross Profit Reality

Three Tiers of Global Appliance Manufacturers

The Zhongyuan Securities report reveals a clear three-tier structure among global home appliance companies based on 2024 gross margins:

Tier 1: Technology Leaders (45–55% gross margin)

– Roborock (石头科技): 55.1%

– Robam (老板电器): 48.7%

– Ecovacs (科沃斯): 47.5%

Tier 2: Scale Leaders (25–32% gross margin)

– Daikin Industries: 32.6%

– Haier Smart Home (海尔智家): 26.4%

– Midea Group (美的集团): 26.2%

– Gree Electric (格力电器): 29.4%

Tier 3: Margin-Compressed Legacy Players (14–22% gross margin)

– LG Electronics (Home Appliance Division): 18.9%

– Panasonic (Home Appliance Division): 18.5%

– Whirlpool: 16.8%

– Electrolux: 14.2%

The most striking observation: established Japanese, American, and European appliance giants cluster in the lowest tier. Squeezed by Chinese supply chain advantages and aggressive pricing, these legacy players continue to struggle with margin compression.

Five Factors Driving Margin Differentiation

The report identifies common factors that separate high-margin players from the rest:

- Technical barriers and product differentiation: Companies with proprietary algorithms and AI capabilities command premium pricing

- Brand premium power: Premium brands consistently achieve higher margins than mass-market competitors

- Vertical integration depth: In-house production of core components like compressors and motors directly improves profitability

- Globalization and channel costs: International expansion drives growth but can erode margins through distribution expenses

- AI premium: Products incorporating artificial intelligence generate higher value-add and represent new profit engines

Strategic Implications for International Businesses

Career Considerations

The expansion of China’s smart appliance market creates direct implications for professionals in adjacent industries:

-

Product planning and marketing roles: The penetration gaps in dishwashers and robot vacuums indicate substantial opportunity to reach Chinese consumers with underpenetrated products. Demand is rising for marketers and product managers who understand Chinese consumer pain points.

-

Technology roles: Engineers with expertise in Matter protocol (the emerging smart home interoperability standard) and AIoT platforms are in high demand across Chinese startups and global multinationals alike.

-

Supply chain and procurement roles: Professionals with deep knowledge of China’s Shenzhen-centered appliance component clusters have become essential to global appliance manufacturers’ operations.

Business Strategy Recommendations

Three actionable priorities emerge for companies competing in or adjacent to this space:

① Avoid undifferentiated competition; focus on defensible strengths

The margin data makes clear that competing on scale alone leads to crushing pressure from Chinese supply chain advantages. Companies like Panasonic and Sony demonstrate that sustainable positioning requires combining technology leadership with brand premium in specific categories—cooking appliances, premium HVAC systems, and similar segments where differentiation matters.

② Transform Chinese companies’ global expansion into partnership opportunities

Haier’s acquisition of Western brands and Roborock’s 17%+ market share in Europe and North America signal that Chinese brands are accelerating international expansion. Rather than viewing this solely as competitive threat, international companies should evaluate OEM arrangements, technology licensing, and distribution partnerships.

③ Monitor AI integration in home appliances closely

Generative AI is now being embedded in consumer appliance platforms. Combined with Matter protocol adoption, the “whole-home smart” concept may achieve mainstream penetration faster than current forecasts suggest. Companies that successfully ride this wave will secure competitive advantages for the next three to five years.

Key Takeaways

-

The global smart appliance market will reach $180 billion in 2026. Chinese brands lead with 38–40% of shipments and are transitioning to a new competitive phase centered on AI and whole-home integration.

-

Massive “smart gaps” remain in China’s domestic market. Robot vacuum penetration (4.2%), dishwashers (5%), and AI kitchen appliances (24%) all lag significantly behind U.S. levels, creating blue-ocean growth opportunities for the coming years.

-

Margin gaps reflect technology and brand differentiation. The 30+ percentage point spread between China’s technology leaders (Roborock at 55%) and legacy international players (LG at 18.9%, Panasonic at 18.5%) will persist unless companies successfully leverage AI and differentiation to escape price competition.

→ Related: China Smart Home Market Trends | China AI Industry Report | AWE 2026 Highlights

Leave a Reply